3 Key Pricing Strategies For Monetising Payments

A successful monetisation strategy can boost your software companies’ ARR by up to 2 to 5 times. Read on to find out how to create a pricing strategy for payments that suits your business and will generate a maximum return on investment.

What makes a monetisation strategy successful?

The best monetisation strategies are:

- Competitive within your industry

- Non-intrusive and fits in with your clients’ existing payment flow

- Does not impede on your client’s business

- Suits your business infrastructure

- Generates a maximum profit for your business

- Flexible and can change as your business grows

- Can be applied to a variety of payment methods and channels for maximum exposure

There are multiple ways to monetise your payments infrastructure and increase your cash flow through payments. However, there are caveats with selling payments to your customers. It’s important to explore the compliance requirements before setting anything in stone or taking it to market.

Without an Australian Financial Services License (AFSL), you cannot legally set pricing or sell payments to your merchants. However, if you partner with an existing payment facilitator, you can still customize your payments strategy with the help of your payments partner.

When considering how you can monetise your payments, it’s a good idea to consult with a payments expert as well as compare with your competitors’ pricing in the industry to ensure you can stay competitive.

If you partner with an existing Payment Facilitator through an embedded or integrated model, you can leverage their experience and expertise to create the most beneficial structure for your company and target audience.

There are generally 3 main strategies or options to consider when monetising your payments:

1. Charge A % Fee For Transactions Processed Through Your Platform

This works if you:

- Have clients that process frequent or recurring transactions

- Have clients that accept large transaction amounts infrequently

- Can take a variety of payment methods

- Can customise your transaction fees to include a surcharge

If your software customers are businesses that process frequent transactions and have a relatively large number of recurring customers, then this is by far the most profitable and least intrusive way to generate income from payments.

By charging a small transaction % fee for processing payments, you can create ongoing recurring cash flow, without having to ask your customers to commit to upfront pricing plans or bulk fees.

There are two ways you can do this – either by becoming your own PayFac or partnering with a specific type of payments provider that offers revenue share agreements. Some payment providers (like Payrix) will give you a revenue share by providing payments at a wholesale rate and allowing you to add a margin per transaction fee.

This means you can still generate a profit from every transaction (like you would if you were a PayFac) but at a slightly lower rate. However, you also face significantly less costs to get up and running.

Payment fees are often complex and layered, so it’s best to speak to a payments expert to uncover the ‘true costs’ of your payments. For example, things like refund fees, late fees, chargeback fees, and failed payment fees can quickly rack up your costs. At Payrix, we combine the inherently complex pricing from banks into a simple, wholesale rate for our partners.

example

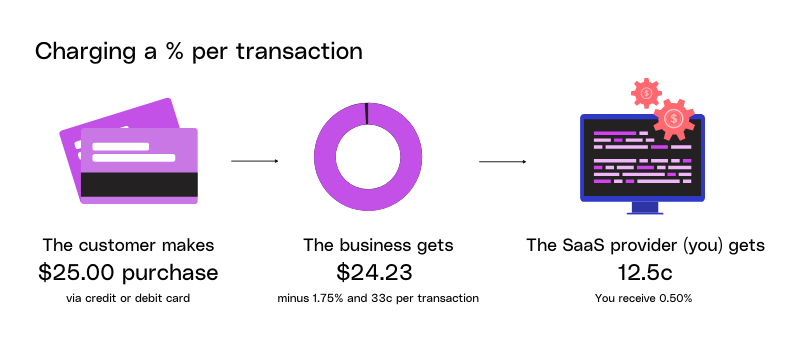

Fitness Management Platform Surcharges Membership Transactions

You are a fitness management platform that caters for gyms, swim schools and fitness centers. Your customers/users are businesses that have weekly, fortnightly, or monthly membership arrangements with their customers.

You decide you want to generate a 0.50% profit on top of every transaction. In this scenario, your provider is charging 1.25% per transaction (including bank fees). Therefore, you work with your payments partner to set the total fee to be 1.75% per transaction. *

In this scenario, your customers’ members make an average purchase price of $25.00, of which you are generating a 12.5c profit (based on taking 0.50% of the transaction) by enabling the payment to be processed through your software.

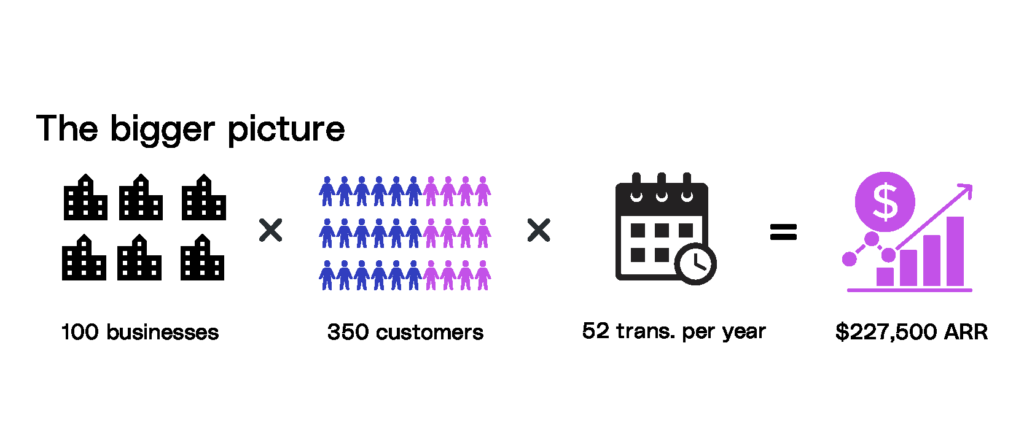

More payments volume = more revenue

12.5c may not seem like a lot at first glance, but enabling payments is a volume game. Consider you have 100 businesses that are using your software, each with an average of 350 customers, who make an average of 52 purchases per year. At an average purchase price of $25.00, your 0.5% transaction fee would equal over $220K in extra revenue per year!**

KEY TAKEAWAYS

- Set a % margin that is competitive and not too high

- This monetisation strategy works best for software companies that have a high volume of customers, with frequent transactions

- This model is the least intrusive way to monetise payments as it does not require any upfront commitment or bulk fees from your customers

- Consider hidden fees like late fees, refund fees, and failed payments when weighing up your provider and setting your % fee

*This is an example of surcharging, and is a regulated practice that must be set by a registered provider (i.e. your payments partner). There are regulations governing surcharging that must be met, including the Cost of Acceptance regulations. **This is an example only and is not an accurate calculation for your specific business case. Speak to a payments expert for more details.

WANT TO SEE MORE?

Download The Full Payments Guide

Curious to find the best strategy for monetising your payments? Download our full payments guide to see all three strategies, as well as useful insights on weighing up costs vs. profit.

Download Now